- Home

- Home Loans

- News

- Home loan intentions have plummeted in the last 12 months

Home loan intentions have plummeted in the last 12 months

Intention to take out a home loan has fallen off a cliff in the last twelve months, dropping 17.7 per cent, according to research by Roy Morgan.

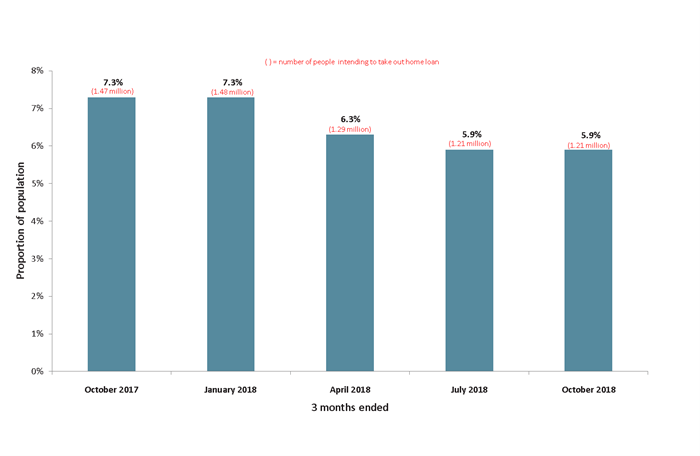

Roy Morgan research found that in the three months to October 2018, 1.21 million Aussies had intentions to take out a home loan. This is a decline of 260,000 people from the 1.47 million recorded in the same time frame in 2017.

Intention to take out home loan in next 12 months

Source: Roy Morgan Australia

2018 started strong for home loan intention levels, with the January quarter at 1.48 million people (7.3 per cent of the population). However, by the 2018 April quarter this had declined to 1.29 million people, a fall of 12.8 per cent. The 2018 July and October quarters fell further by 5.9 per cent (1.21 million people).

This may prove to be a big problem for banks, whose profit margins will be squeezed while they try to bring in new customers over the next twelve months.

Intention to take out home loan in next 12 months – by type of intender

Source: Roy Morgan Australia

Roy Morgan research has pointed to a decline in first home buyer intention levels as the main cause for this fall.

“In the October 2018 quarter only 411,000 first home borrowers intend to take out a loan in the next 12 months, this is down by 44.5 per cent on the 740,000 recorded a year earlier.”

The largest segment in the October 2018 quarter who currently have intention to take out a home loan are existing borrowers looking to refinance (45.4 percent, or 549,000 people).

Further, the largest increase from any segment with intention to take out a home loan was with Australians who have had a loan in the past but wish to move and take out a loan. They grew by 64,000 people to 249,000 – an increase of 34.6 per cent in the twelve months leading to the October 2018 quarter.

Norman Morris, Industry Communications Director, Roy Morgan says believes the overall rate of decline is “likely to have a major impact on banks in the coming year.”

“Particularly as the drop has come from first home buyers who are major generators of increasing volumes.

“The reduction in first home buyers is likely to come from a number of potential reasons, including uncertainty as a result of declining housing values, likely interest rate movements, mortgage stress and job risks.

“The current high level of negative publicity given to borrowing by the Finance Royal Commission is also likely to be impacting on both the supply and demand for home loans.

“The potential for the tightening of lending criteria and issues relating to mortgage brokers are just some of the likely issues to have a negative impact in this market,” said Mr Morgan.

Disclaimer

This article is over two years old, last updated on November 21, 2018. While RateCity makes best efforts to update every important article regularly, the information in this piece may not be as relevant as it once was. Alternatively, please consider checking recent home loans articles.

Compare home loans in Australia

Product database updated 19 Apr, 2024

Share this page

Get updates on the latest financial news and products

By continuing, you agree to the RateCity Privacy Policy, Terms of Use and Disclaimer.

{kind=link}