- Home

- Media Room

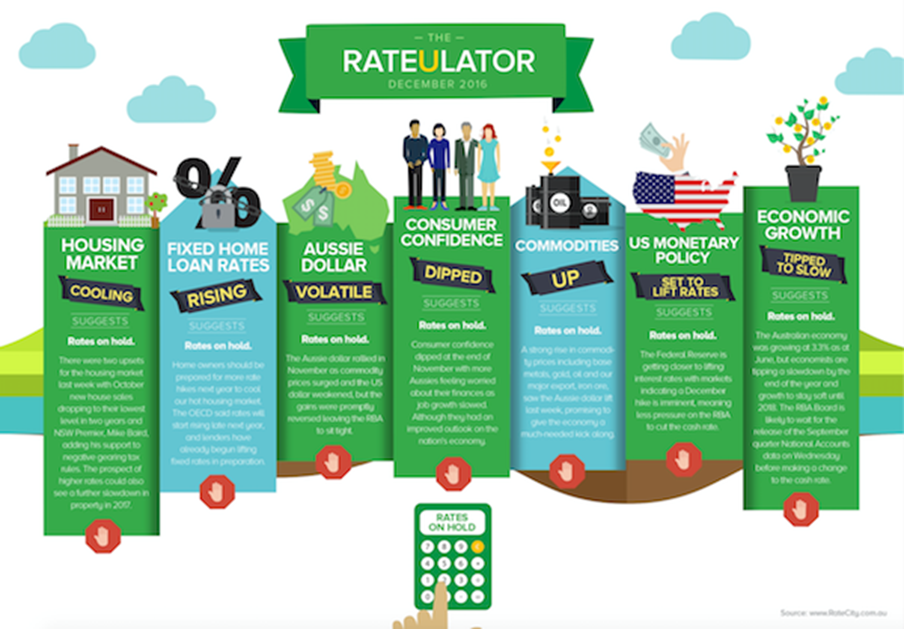

- Rates to hold in December, before rising in 2017

Rates to hold in December, before rising in 2017

Updated on

December 5, 2016: Official interest rates are poised to hold at the historic low of 1.50 per cent when the Reserve Bank Board meets this Tuesday.

But a RateCity.com.au analysis of over 30 key economic indicators suggests the easing cycle has ended.

Peter Arnold, data insights director at RateCity.com.au said the chances of a rate hike in 2017 were mounting.

“Australians should get ready for rates to go up next year to cool our hot housing market,” he said.

“The banks have already started moving fixed rates higher; with Westpac the first major bank to move, along with another 22 lenders which have hiked some of their home loan rates.

“With that many lenders moving fixed rates up, it’s the best sign that we have that a variable hike is on the way.”

Warnings came from leading international forecasters, including the OECD, which said the hikes are needed to “unwind tensions from the low-interest environment, notably in the housing markets”.

Arnold said there were two upsets for the housing market last week.

“New house sales have dropped to their lowest level in two years and NSW Premier, Mike Baird, added his support to negative gearing tax rules,” he said.

“The good news is that the unemployment rate is set to stay low and economic growth is strong, as are commodity prices.

“The Federal Reserve is getting closer to lifting interest rates with markets indicating a December hike is imminent, meaning less pressure on the RBA to move with urgency. Nevertheless, we think a rate hike is likely for next year.”

Please feel free to use the below infographic. For commentary please get in touch, or for a high-resolution version click here.

Share this page

{kind=link}

Did you find this page helpful?

^Words such as "top", "best", "cheapest" or "lowest" are not a recommendation or rating of products. This page compares a range of products from selected providers and not all products or providers are included in the comparison. There is no such thing as a 'one- size-fits-all' financial product. The best loan, credit card, superannuation account or bank account for you might not be the best choice for someone else. Before selecting any financial product you should read the fine print carefully, including the product disclosure statement, target market determination fact sheet or terms and conditions document and obtain professional financial advice on whether a product is right for you and your finances.