- Home

- Home Loans

- News

- Mortgage arrears on the rise as savings in offsets decline

Mortgage arrears on the rise as savings in offsets decline

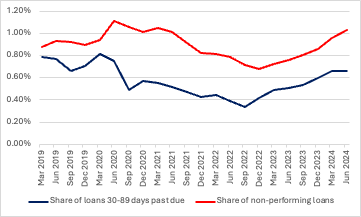

The value of home loans in arrears by 30 to 89 days has risen for the seventh consecutive quarter, as borrowers struggle to keep on top of repayments.

It now stands at $14.88 billion according to the latest APRA Quarterly ADI Property Exposure statistics data, released for the June 2024 quarter.

This amount is a slight increase of $202.1 million, or 1.38 per cent, on the March quarter, however, it is a staggering $5.93 billion, or 66.3 per cent higher than before the RBA rate hikes (March 2022 quarter).

While it now stands at 0.66 per cent of all credit outstanding, this is still, on average, below what it was in the year before COVID at 0.73 per cent.

In 2019, the share of non-performing loans was, on average 0.91 per cent. Today, it stands at 1.03 per cent, after increasing over the last six quarters.

Non-performing loans as a proportion of credit outstanding

Source: APRA Quarterly ADI Property Exposure statistics. Based on all authorised deposit-taking institutions, excluding payment facilities and specialist credit card providers.

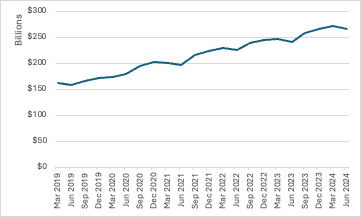

Meanwhile, the total amount of money stashed in offset accounts has dropped by $6.14 billion to $265.58 billion, as borrowers dip into savings as cost of living pressures rise.

Despite the dip, this amount is $37.53 billion higher than it was before the rate hikes began, according to APRA for the June 2024 quarter.

This is the first quarter that offset balances have dropped in the past year. However, since March 2019, APRA has recorded a drop in offset balances in all June quarters, except one (June 2020), followed by a rise in the September quarters.

Offset balances now account for 10 per cent of credit limits owing across the mortgage books of authorised deposit-taking institutions.

Total amount in residential offset accounts

June 24 quarter | Change from previous quarter | Change since RBA hikes (March 2022 quarter) |

$265.58 billion | -$6.14 billion | +$37.53 billion |

Source: APRA Quarterly ADI Property Exposure statistics. Based on all authorised deposit-taking institutions, excluding payment facilities and specialist credit card providers.

Balances in offset accounts

Source: APRA Quarterly ADI Property Exposure statistics.

New loans stress tested at 9.3%

The average variable rate of loans funded in the June 24 quarter was 6.33 per cent – an increase of around 3.79 percentage points since the start of the rate hikes.

The average rate banks are now stress testing new mortgage applications is at 9.31 per cent.

This is because APRA asks banks to stress test a new borrower’s finances to make sure they can still afford the mortgage if rates were to rise 3 percentage points from the rate they are applying for, although exceptions can be made.

Prior to November 2021, this buffer was 2.5 percentage points.

For someone taking out a $500,000, 30-year mortgage in the June 24 quarter, their repayments would be $3,105. This compares to someone taking out the same loan at the start of the rate hikes, whose repayments would be $1,989– an increase of $1,116 per month.

Cost of borrowing $500,000 June 2024 vs before the rate hikes (March 22 quarter)

Rate | Monthly repayment | Difference | |

March 2022 quarter - start of RBA hikes | 2.55% | $1,989 | |

June 2024 quarter - latest | 6.33% | $3,105 | +$1,116 |

Source: APRA Quarterly ADI Property Exposure statistics.

RateCity.com.au money editor, Laine Gordon said: “Some Australians saddled with mortgages are struggling to keep up with the repayments, as more households fall into arrears.”

“Despite record high levels of savings in the bank, some families are dipping into their offset stash to keep up with rising cost of living pressures,” she said.

“These are worrying signs for borrowers, but let’s not throw the baby out with the bathwater. Non-performing loans accounted for just 1.03 per cent of all credit outstanding in the June 2024 quarter - that’s a slight increase from 0.91 per cent in the year before COVID.

“If that’s you, and you haven’t yet reached out for help, now is the time to pick up the phone. Banks will go to great lengths to help you back onto your feet - the last thing they want is to see you lose your home.

“People wanting to take out a new loan, or refinance, have a steep climb, with the average new loan rate now 6.33 per cent. On top of this, banks will stress test new mortgage applications at a staggering 9.31 per cent on average.

“Someone borrowing $500,000 today would be forking out $3,105 per month in repayments - that’s $1,116 more than if someone took out the same loan at the start of the hikes,” she said.

Compare home loans in Australia

Product database updated 04 Nov, 2025

Share this page

Get updates on the latest financial news and products

By continuing, you agree to the RateCity Privacy Policy, Terms of Use and Disclaimer.