- Home

- Home Loans

- Articles

- How to find your interest rate

How to find your interest rate

Pop quiz, hotshot – what interest rate are you currently paying on your home loan? Could you name it off the top of your head?

Many studies in recent years have found that the majority of Australians with home loans don’t know their home loan’s current interest rate, with CUA stating in February 2016 that 60% of Australians don’t know what rate of interest they’re paying on their mortgage, and UBank finding in December 2015 that as little as 16% of Australians do know their interest rate. This is despite the interest rate having a major impact on any home loan’s affordability.

Before you can start thinking too seriously about refinancing your home loan and getting a better deal, you’ll first need to find out what rate of interest you’re currently paying as a baseline to compare to other offers. Finding this information isn’t always as easy as it sounds.

Home loans for refinancing:

Here are five ways to find the interest rate on your home loan:

Check your lender’s list of rates

Many lenders will have a page on their website dedicated to listing and comparing the different home loans products they currently provide, including information such as interest and comparison rates. If you know the name of your home loan product, you can look it up in the list and see its details, including the interest rate.

It’s worth remembering that not every home loan may be summarised on one of these pages, as lenders create new home loan offers and discontinue old ones all the time. If you’ve had your mortgage for a number of years, it’s entirely possible that your lender isn’t offering that particular deal to new customers any more, or has changed the name of the offer. Or perhaps a loan offer with the same name is currently available, but at different rates and terms to what you originally signed up for, especially if you have a variable rate home loan.

Check your mortgage statement

To help you keep track of what money going into your home loan (and if you have a redraw facility, any money coming back out), your lender will keep records of recent transactions and other updates to your mortgage in the form of statements, much like what you’d find for a more typical bank account. These statements may be sent to you once or twice a year, or even quarterly or monthly, depending on your lender, and include details around how much you’ve borrowed, how much you’re still owing, the remaining home loan term, and of course, your interest rate.

Many lenders initially send your mortgage statements as physical paper copies for compliance reasons, though you often have the option to switch to paperless online statements that can be accessed via internet banking if you prefer electronic records.

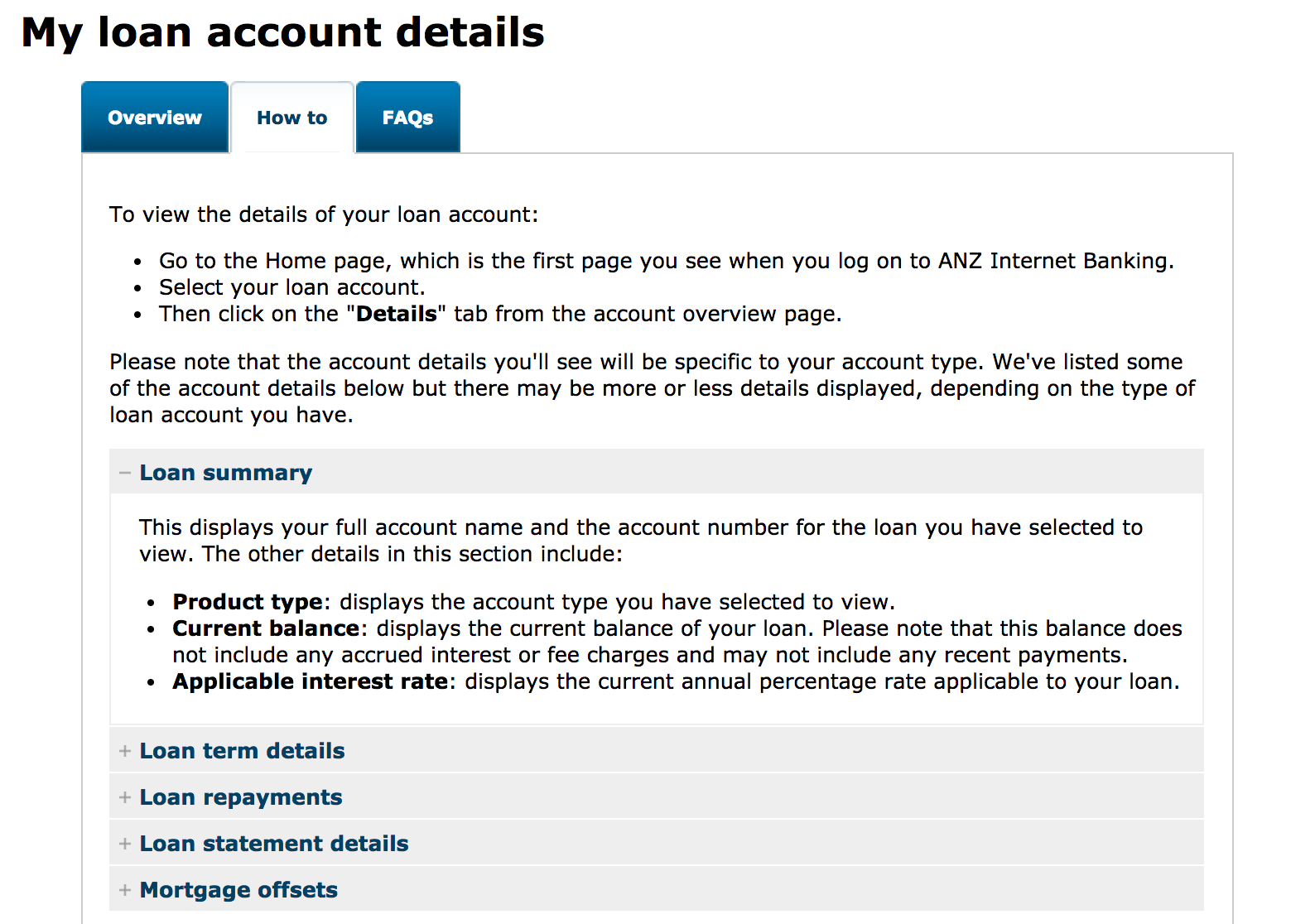

Online Banking

Most lenders include options to conduct most of your banking over the computer, rather than over the phone or in person at a branch. If you have a home loan through one of the smaller non-bank lenders, it’s possible that they conduct ALL of their business online, and don’t have any branches or shopfronts available to visit.

By logging into your online banking, you can usually quickly and easily access basic information about your home loan, such as its current balance. You’ll likely also have the option to transfer extra available cash towards paying off your home loan.

Because lenders often design their online banking services to focus on making day-to-day transactions and transfers smooth and stress-free, rather than providing a lot of extra details, you may need to dig a little deeper into the different tabs and menus to find more detailed information on you home loan, such as its interest rate.

Mobile banking

Finding your home loan interest rate using your lender’s mobile banking app can often follow a similar process to doing so via online banking, with the biggest difference being that you’ll be doing so via your phone rather than on a computer.

Much like internet banking on a computer, mobile banking apps are often designed primarily with simplicity, speed and ease of use for making everyday transactions in mind, so accessing detailed home loan information via your phone may not always be straightforward, depending on your lender.

Calling/visiting them!

Yes, nobody likes waiting on hold, hearing for the thirteenth time that “your call is important to us”, and trying to convince speech recognition software to transfer you to a real person. But sometimes the direct approach is one of the simplest ways to find out your current interest rate.

Make sure you have all of your account information and other details required to confirm your identity handy, and your lender should be able to tell you your home loan’s current interest rate with relatively little fuss.

The same deal goes for visiting a bank branch – if your lender has an office nearby, you can drop in, take a number and wait in line to see if a teller can source your interest rate for you.

What next?

Once you’ve found your current interest rate, what’s the next step towards getting a better deal on your home loan?

Well, assuming you already have a refinancing goal, whether that’s to save money, borrow more, or to pay off your home faster, the next step is to start comparing other home loan offers, both from your existing lender and others, to see if you can find an alternative that will help you reach your lofty goal.

While comparing different home loans by interest rate is important, be sure to compare the other costs, features and benefits too, to make sure that you choose a refinancing home loan that provides great value for your money.

Disclaimer

This article is over two years old, last updated on January 9, 2017. While RateCity makes best efforts to update every important article regularly, the information in this piece may not be as relevant as it once was. Alternatively, please consider checking recent home loans articles.

Compare home loans in Australia

Product database updated 27 Jul, 2024

Fact Checked